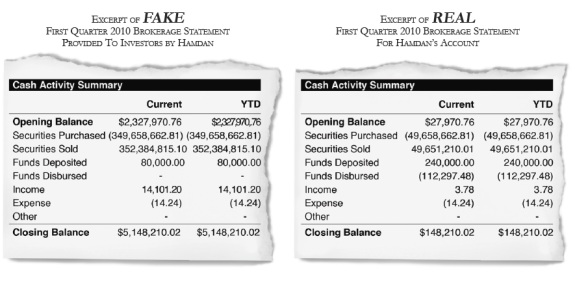

BULLETIN: The SEC has gone to federal court in Houston, alleging that Firas Hamdan was conducting an affinity-fraud scheme targeted at the Lebanese and Druze communities. The agency is seeking an asset freeze against Hamdan and his unregistered company, FAH Capital Partners Inc. The scheme is alleged to have gathered about $6 million over five years.

“Hamdan’s affinity scam preyed upon people’s tendency to trust those who share common backgrounds and beliefs,” said David R. Woodcock, director of the SEC’s Fort Worth Regional Office. “Hamdan raised money by creating the aura of a successful day trader among friends and family in his community, and he continued to mislead them and hide the truth while trading losses mounted.”

Hamdan is 49. The SEC says he has an address in Houston and previously used an address in Sugar Land.

“Hamdan is well-known in the Houston-area Lebanese and Druze communities and has enjoyed a reputation as a successful day trader,” the SEC said in its complaint. “He is also a former treasurer of the Houston branch of the American Druze Society (‘ADS’), a non-profit cultural organization to which many Houston-area members of the Druze religion belong.”

Falsified records helped drive the scam, the SEC said.

As has been the case in other scams, Hamdam allegedly claimed he used a “proprietary trading algorithm.”

“Hamdan explained to investors that his algorithm was ‘plugged into’ his trading account at TD Ameritrade to further minimize investor loss,” the SEC charged. “Hamdan promised investors that, as a result of this algorithm, he could guarantee the fixed monthly return based on the amount they invested with him.”

As has been the case with other scams, Hamdan also talked about “promissory notes.”

“Although the precise terms of the notes appear to vary among investors, the notes generally provide for returns of approximately 30% per year,” the SEC charged.

Fraudsters who carry out affinity scams frequently are (or pretend to be) members of the group they are trying to defraud. The group could be a religious group, such as a particular denomination or church. It could be an ethnic group or an immigrant community. It could be a racial minority. It could be members of a particular workforce – even members of the military have been targets of these frauds. Fraudsters target any group they think they can convince to trust them with the group members’ hard-earned savings.

At its core, affinity fraud exploits the trust and friendship that exist in groups of people who have something in common. Fraudsters use a number of methods to get access to the group. A common way is by enlisting respected leaders from within the group to spread the word about the scheme . . .

URGENT >> BULLETIN >> MOVING: The SEC has gone to federal court in Los Angeles, alleging that a California man was operating a $7.5 million Ponzi scheme targeted at the Persian-Jewish community.

U.S. District Judge Jacqueline H. Nguyen has issued an emergency asset freeze.

Charged in the alleged affinity-fraud caper was Shervin Neman, 30, of the Century City area of Los Angeles. Neman, according to the SEC, formerly was known as Shervin Davatgarzadeh. He presided over an entity known as Neman Financial LP, which the agency described as a “purported hedge fund.”

It was the second major affinity-fraud case announced by the SEC in the past 24 hours. The agency said yesterday that Ephren W. Taylor II, 29, of New York, was operating an $11 million Ponzi scheme targeted at African American church congregations. Taylor was charged in Atlanta.

The Scheme Aimed At The Persian-Jewish Community

“Neman deceived members of his own community to raise money in this fraudulent Ponzi scheme,” said Michele Wein Layne, associate regional director of the SEC’s Los Angeles Office. “By exploiting investors’ trust in him, Neman was continually able to raise more money to pay back existing investors and finance an extravagant lifestyle.”

The Neman Ponzi married a real-estate flipping scheme involving purported foreclosures to purported opportunities to profit from IPOs conducted by Facebook , Groupon, LinkedIn and Angie’s List, the SEC said.

“Although Neman promised investors exorbitant returns resulting from his investing acumen and access to pre-IPO shares of well-known companies, what they actually received was simply other investors’ money in hallmark Ponzi scheme fashion,” the agency said.

Named a relief defendant in the case was Neman’s wife, Cassandra C. Neman, 33. She is not charged with wrongdoing, but the SEC said she received gifts from her husband, including a $60,000 ring, that were paid for from Ponzi proceeds.

Neman’s investors also were paying for his wife’s personal expenses, the SEC said. The Nemans wed in October 2010. The fraud scheme may date back to June 2010. It allegedly raised at least $7.54 million from investors in California, Florida and Texas, the agency said.

More than 99 percent of investors’ funds were directed either to Ponzi payments or to prop up Neman’s tony lifestyle, the SEC said.

“Specifically,” the agency said, “of the $7.54 million raised from investors since June 2010, Neman has used more than $5.4 million to make Ponzi payments to existing investors, and has spent another nearly$1.6 million to support a lavish lifestyle and maintain the appearance of an upscale

business operation. Due to recent investments from new and existing investors,Neman owes nearly $2.7 million in principal payments alone to his investors.”

Neman filled his personal bank account with investors’ money, the SEC said.

“In most instances, Neman directed investors to wire their funds to a personal bank account held in Neman’s name or to write checks to him personally, which he then deposited into his personal account,” the SEC charged. “Neman commingled investor funds in his personal account.”

As was the case yesterday in the SEC’s allegations against Taylor in the alleged affinty-fraud scheme targeted at Christians, the agency said today that Neman’s fraud involved promissory notes.

Neman was operating a straightforward scam, the SEC said.

“Among other things, Neman used investor funds to pay for his wedding and honeymoon, his wife’s engagement ring, luxury cars, VIP tickets to entertainment venues, jewelry, hotels, and restaurants,” the SEC charged. “Neman also used investor funds to lease and redecorate a new office in an upscale building in the Century City area of Los Angeles, hire two administrative assistants, and pay legal and other professional expenses . . .”

“Ephren Taylor professed to be in the business of socially-conscious investing. Instead, he was in the business of promoting Ephren Taylor. He preyed upon investors’ faith and their desire to help others, convincing them that they could earn healthy returns while also helping their communities.” — David Woodcock, director of the SEC’s Fort Worth Regional Office, April 12, 2012

Ephren W. Taylor II: From: YouTube

URGENT >> BULLETIN >> MOVING: The SEC has gone to federal court in Atlanta, alleging that well-known speaker Ephren W. Taylor II was at the helm of an $11 million Ponzi scheme targeting African American church congregations through two investment “programs” offered by City Capital Corp.

Taylor is 29, the son of a minister. Taylor last was known to be living in New York, but [h]is current whereabouts are unknown,” the agency alleged.

“He failed to respond to a number of Commission investigative subpoenas, including a subpoena requiring his appearance for testimony,” the agency advised a federal judge in a complaint filed in Atlanta.

Former City Capital COO Wendy Jean Connor, 43, of metropolitan Raleigh, N.C., also was charged in the alleged caper. The agency said that she pocketed “hundreds of thousands of dollars” in salary and commissions that came from money investors plowed into the Ponzi, which was at least in part a promissory-notes scam married to a “sweepstakes machine” business and other purported businesses.

Taylor “secretly” funded his wife’s singing career with Ponzi money and “diverted hundreds of thousands of dollars to publishing and promoting his books” and “hiring consultants to refine his public image,” the SEC charged.

The scheme was multifaceted and occurred across multiple jurisdictions, with Taylor focusing on African Americans, denigrating traditional investment options and encouraging his audience to plow money from their Individual Retirement Accounts into his schemes, the agency charged.

The ‘Building Wealth Tour’

“Taylor conducted a multi-city ‘Building Wealth Tour,’ on which he spoke to church congregations — including Atlanta’s New Birth Church — or at wealth management seminars featuring other speakers,” the agency charged. “Taylor promoted the Building Wealth Tour on his personal website, through City Capital press releases, and in conjunction with the churches and civic groups that hosted him. Taylor heavily emphasized his Christian background . . . and, indeed, was at times referred to as ‘Minister Taylor.’

“He also touted his ‘socially conscious’ investment focus and successful entrepreneurial history,” the agency continued. “Taylor devoted considerable time to denigrating traditional investment vehicles, such as CDs, mutual funds and the stock market, labeling them as ‘foolish’ and ‘money losers.’”

One of his scam websites was styled SweepstakesIncome.com, the agency alleged, further alleging that the purported investment opportunity was positioned as the “brainchild of self-made millionaire Ephren Taylor.”

Part of the pitch “featured Taylor’s lengthy dissertation about ‘How You Can Create a Zero-Maintenance, Residual Income Using the Sweepstakes Empire!’” the agency alleged.

Priming The Ponzi

To prop up the multifaceted Ponzi, the SEC alleged, investors were encouraged to “roll their notes over” for another year or longer — with corresponding promises that delaying redemptions would “increase the rate of return,” the SEC charged.

“The roll-over solicitations typically touted the supposed ‘great things — usually of a socially conscious nature — City Capital was doing with the investor’s money, which were all untrue,” the SEC charged. “Investors who renewed were issued new promissory notes with the new term and interest rate. Any investor who resisted was subjected to an endless cycle of unreturned phone calls and emails, empty promises of imminent action, and claims that the investor had in fact already agreed to roll over his note. To the extent investors survived this gauntlet to still insist on repayment, any funds they received invariably came from new investor money.”

Undisclosed Risks

Meanwhile, the SEC alleged today that schemes involving sweepstakes machines already were on the radar of law enforcement even as Taylor dialed up his efforts to get investors to send him money.

“Offering materials stressed that the sweepstakes machines did not involve gambling, comparing them to McDonald’s ‘Monopoly’ prize game,” the SEC charged. “Investors were not told about the risks of illegality of the machines, or that several law enforcement agencies had taken action against City Capital’s and other parlors.”

Investors paid up to $4,497 per machine, amid claims City Capital had purchased and established several ‘internet cafes’ featuring the machines,” the SEC alleged.

City Capital paid employees a commission of 10 percent for selling the machines, and Taylor and Connor were paid “overriding commissions of 10% per machine,” the SEC charged.

All in all, the sale of sweepstakes machines raised at least $4 million from more than 250 investors, the agency charged.

Returns From ‘Thin Air’

In April 2010, the SEC charged, “City Capital’s bookkeeper alerted Taylor and Connor to the weak performance of the company’s recently acquired North Carolina and Texas parlors, explaining that the locations each suffered a loss after deducting operating expenses.

“Rather than tell investors assigned to machines in those locations that they would get no distributions — perhaps to avoid an investor backlash — Taylor and Connor instructed the bookkeeper to pay simulated returns essentially pulled from thin air,” the SEC continued.

“The bookkeeper had to divert funds received from new sweepstakes machine investors — and from investors’ funds in other City Capital ventures — to make these payments,” the agency charged. “As the parlors continued to lose money over the ensuing months, Taylor and Connor instructed the bookkeeper to continue making these simulated payments, telling her simply to make the same payment ‘as last month.’ These payments ended after August 2010, when City Capital ran out of money.”

UPDATED 7:43 A.M. ET (MARCH 9, U.S.A.) If ever there has been a cautionary tale for HYIP pitchmen, it is Jeffrey Lane Mowen’s Utah Ponzi scheme.

Mowen and at least six promoters ended up inspiring litigation on multiple fronts, with Mowen charged criminally. At issue was Mowen’s Forex Ponzi scheme, which allegedly was funded in part through an alleged high-yield “promissory notes” offering fraud.

Tonight, Mowen, 49, is listed as “in transit” to an unspecified federal prison. He has been jailed in the United States since he was extradited from Panama in 2009. He pleaded guilty to U.S. charges of wire fraud last year and was sentenced to 10 years.

Mowen received a merciful plea agreement in which other serious criminal charges were dropped, including solicitation to commit a crime of violence, witness tampering and retaliating against a witness.

The sidebars in the Mowen story have been every bit as compelling as the story-in-chief. Indeed, Mowen sought to shield himself in Panama when his scheme collapsed.

It didn’t work. Panamanian authorities and the FBI got him quickly.

Jeffrey Lane Mowen

After his return to the United States, Mowen allegedly solicited the murder of four witnesses “with the intent of preventing their attendance and testimony at his federal fraud trial” in the Ponzi scheme case.

That didn’t work. The cellmate through whom he allegedly solicited the murders was a snitch.

But the cautionary tale doesn’t end there. Jeffrey Lane Mowen was a felon and a recidivist securities huckster. Thomas Fry, an unregistered promoter, used at least five other unregistered promoters to raise funds for “opportunities” that purported to pay a return of between 2 percent and 3 percent a month, according to the SEC.

Fry and the pitchmen were sued by the SEC in 2009. All six also now face administration sanctions from the SEC — this after the agency targeted their ill-gotten gains in the earlier lawsuit.

Failure to conduct due diligence and engaging in willful blindness were elements in the SEC’s lawsuit 2009 against the promoters, according to court filings.

“Because the Promoters not only conducted virtually no due diligence in connection with Fry’s purported investment opportunities, but transferred investor money to Fry without any documentation or limitation on his use of the funds, the Promoters were reckless in failing to discover Fry’s association with Mowen and that their funds were being placed into a Ponzi scheme or used for other undisclosed purposes,” the SEC charged at the time.

All of the pitchman now have been barred from the securities business under the terms of the administrative action. In a settlement, none of the pitchmen acknowledged wrongdoing. But the various Ponzi- and fraud-related actions were front-and-center in their lives for the better part of three years.

This common paragraph appears in each of the administrative actions against the five Fry pitchmen (italics added):

“The Commission’s complaint alleged that, from at least January 2007 through July 2008, [Pitchman’s Name] offered and sold purported high-yield promissory notes to investors that he claimed would pay 2% to 3% interest monthly. The funds raised by [Pitchman’s Name] were given to Thomas R. Fry who funneled those funds into a Ponzi scheme run by Jeffrey L. Mowen, a convicted felon and securities law recidivist. The Commission alleged that [Pitchman’s Name] distributed private placement memoranda to investors that falsely stated that all the investors’ funds were being used to make collateralized domestic real estate loans and domestic small business loans and that misrepresented the level of his due diligence as to the investment scheme. The Commission alleged that [Pitchman’s Name] conducted virtually no due diligence in connection with the purported investment opportunities and transferred investor money without any documentation or limitation on the use of the funds.”

Fry knew Mowen was a scammer, but still continued to solicit funds, the SEC said. All in all, he and the other five pitchmen raised more than $18 million for Mowen.

But the FBI said Mowen wasn’t operating a legitimate investment opportunity. What he was doing was buying exotic cars, taking personal vacations, supporting a luxurious lifestyle and making Ponzi payouts that ultimately defrauded more than 200 investors out of between $9 million and $10 million.

The purported monthly returns offered by JSS Tripler/JustBeenPaid — an “opportunity” now making its way around the web — are roughly TWENTY times higher than the scheme pitched by Fry and his promoters, according to records.

As noted above, the alleged offering fraud involving Fry and the other pitchmen was promoted on the purported basis of returns of 2 percent to 3 percent a month. JSS Tripler/JustBeenPaid advertises 60 percent a month.

Also on a monthly basis, the purported payout of JSS Tripler/JustBeenPaid is roughly between TWO and SEVEN times higher than the payout of the Ponzi scheme that put Mowen in prison for 10 years, according to records.

Mowen’s Forex Ponzi scheme scheme offered between 8 percent and 33 percent a month, federal prosecutors said last year.

It is somewhat common for HYIP purveyors who populate Ponzi boards such as TalkGold and MoneyMakerGroup to assert they have conducted “due diligence” on an “opportunity” or to assert that a “program’s” operator and/or management “team” have done so and that prospects don’t have to concern themselves with doing any legwork.

It often proves to be the case that the “due diligence” consists of GIGO — garbage in, garbage out. The promoters simply repeat the company line, rather than doing any sort of critical assessment such as questioning how an HYIP “program” operator could provide returns that may dwarf the returns of Bernard Madoff and other Ponzi schemers such as Mowen.

AdSurfDaily figure and purported “sovereign citizen” Kenneth Wayne Leaming has pleaded not guilty to all six felony counts contained in a grand-jury indictment returned Jan. 26.

U.S. Magistrate Judge Karen L. Strombom presided over Leaming’s arraignment at 1:30 p.m. PT in Tacoma, Wash.

Leaming, 56, of Spanaway, Wash., remained in federal custody after the proceeding. His trial date on three counts of Retaliating Against a Federal Judge or Law Enforcement Office by False Claim and single counts of Concealing a Person from Arrest , Felon in Possession of a Firearm and False and Fictitious Instruments was set for March 20.

Leaming has been detained near Seattle since his initial arrest in November 2011. Prosecutors said he was found with two federal fugitives from Arkansas and at least six weapons. The fugitives — Timothy Shawn Donavan, 63, and Sharon Jeannette Henningsen, 67 — now are listed as federal inmates at facilities in Texas.

Donavan and Henningsen initially were freed on bond several days after their arrests with Leaming in Washingston state. After returning to Arkansas, trouble soon followed, and they were ordered back into federal custody for violating bond conditions.

Leaming, who has a 2005 felony conviction for piloting an aircraft without a valid pilot’s certificate, is accused of filing false liens against several public officials, including at least five officials involved in the AdSurfDaily Ponzi case.

He initially was detained in November on the false-liens charges. A grand jury later added the firearms charge, the concealment charge related to Donavan and Henningsen and the charge of false and fictitious instruments. That charge stemmed from the alleged issuance by Leaming of a bogus “bonded promissory note” with a purported face value of $1 million, according to the indictment.

Richard Elkinson, the 78-year-old Ponzi swindler whose promissory notes scheme gathered $29 million over 20 years, has been sentenced to 102 months in federal prison.

Elkinson resided in Framingham, Mass., and told investors he was in the business of providing uniforms to the government and other entities.

But it was all a scam that lured investors with promises of outsize returns of between 9 percent and 15 percent in less than a year, federal prosecutors, the FBI and the SEC said.

The scheme began to collapse in late 2008 after investors — motivated by the publicity the Bernard Madoff Ponzi began to receive — “started seeking more information and documents about the uniform business,” the office of U.S. Attorney Carmen M. Ortiz of the District of Massachusetts said yesterday.

Madoff, himself a senior swindler at the helm of a long-running Ponzi caper, was arrested on Dec. 11, 2008.

Although Elkinson initially lulled investors in early 2009 with a variety of excuses about why he wasn’t making payments, he later fled Massachusetts. Elkinson was arrested at a Mississippi casino in January 2010. Investigators said they discovered evidence that the con man had an affinity for gambling and had conducted “a total of more than $3.7 million in currency transactions over $10,000” at Las Vegas casinos dating back to 1998.

Screen shot: PDF from section of Page 1 of the indictment of Doris E. Nelson in an alleged $126 million Ponzi operating internationally through multiple companies.

EDITOR’S NOTE: This information is presented in the form of briefs, with links to external sources.

1.)Doris E. Nelson, arrested/jailed in Spokane, Wash., region, last week after federal raid in April 2010. SEC filed civil charges in September 2011.

The allegations against Nelson and multiple companies in Nevada, Utah and Canada are alarming, but also somewhat standard fare if you’ve been observing how schemes form and then explain away problems when trouble develops.

Among the core allegations are these:

Nelson, of Colbert, Wash., ran a payday-loan business called “The Little Loan Shoppe” in the area of Spokane. The firm was linked to multiple LLCs in the United States and multiple LTDs in Canada. The business started out in the Canadian province of British Columbia in roughly 1997, and moved to the United States “in or about 2001.” Investors were told they could earn enormous profits from the spread between the loan shop’s expenses and what it charged customers for a short-term loan.

The Ponzi scheme took in “at least” $126 million and caused losses of more than $40 million — losses that affected “at least” 800 investors.

Federal prosecutors say they have identified “victim investors” in multiple Canadian provinces and multiple U.S. states. The indictment also lists a victim from Spain.

The payday loan business was not profitable. Investors were getting paid through a complex shell game that lasted for years and involved the formation of new companies, including marketing and “leads” arms.

Nelson and some of the defendants engaged in wire fraud, mail fraud and money-laundering.

Nelson lied to the Manitoba Securities Commission and advised certain parties to lie to the British Columbia Securities Commission (BCSC).

Nelson used investor funds to purchase a motor home valued at nearly $127,000, a Chevrolet Corvette valued at more than $61,000, a Mercedes Benz valued at nearly $112,000. She purchased more than $220,000 in clothing at the St. Johns Knits store and $217,000 at other stores, including Nordstrom.

Nelson lost $400,000 of investors’ funds gambling at various Las Vegas casinos.

Nelson spent investors’ money on luxury sea cruises, including nearly $29,000 on a Royal Caribbean cruise in which she also spent $23,500 in investor funds to gamble.

The promissory-notes scheme showed classic signs of collapse in October 2008. (More details below.) Nelson slashed payouts to investors — from an anticipated rate of between 40 percent and 60 percent to 10 percent. The 10 percent payouts collapsed by March 2009.

Nelson claimed Little Loan Shoppe bought the building it used in Spokane, but that was a lie. In truth, the company was paying rent to a company owned by Nelson’s husband.

In February 2008, leading up to the beginning of the end in October 2008, Nelson forecast “an explosion of profit.” In May, she announced that “our industry is thriving.” She then opened a new window for investments, telling marks that she was “excepting” new money, as opposed to “accepting” it. “[T]his window of opportunity will probably not be open again due to the expected surplus of income . . .” she wrote.

Between late June and late July of 2008, Nelson announced a “massive marketing campaign” that would turn the operation into “one of the largest loan companies.”

Millions of dollars flowed to the teetering scheme after Nelson’s various hype fests.

In October 2008, Nelson lied to BCSC about how she was making interest payments to investors, denying that the money came from “newer” investors and claiming the cash came from loan profits.

BCSC ordered Nelson to stop issuing promissory notes. Nelson then told investors that changes to U.S. lending laws had “dramatically reduced our profits . . .”

In February 2009, Nelson advised investors to quit contacting her about their investments because the inquiries were distracting her. She then announced a purported account review. In March 2009, Nelson told investors that the account review was behind schedule and perhaps would not be completed until the middle of April.

In March 2009, Nelson traveled to Florida to try to get more money from existing investors.

The scam then collapsed in its entirety and investors experienced ruin.

Read/view coverage of alleged Nelson scam at KXLY.com.

The Alleged Garfield M. Taylor Ponzi Scheme In Metro Washington, D.C.

2.)Garfield M. Taylor, others sued by SEC last week amid spectacular allegations of Ponzi fraud targeted at charities and people of faith, among others.

Outlined below are some of the core allegations in the alleged Garfield M. Taylor Ponzi scheme, which includes multiple defendants and multiple companies. The SEC brought the case last week, alleging a $27 million Ponzi scheme.

First, a quote from Stephen L. Cohen, the SEC’s associate director in the Division of Enforcement.

“Garfield Taylor and his partners in the scheme touted themselves as seasoned and trustworthy financial professionals offering a conservative but lucrative investment opportunity. In reality, they were gambling away investor assets in extremely risky trades and operating a classic Ponzi scheme.”

Key allegations:

Garfield Taylor, of North Bethesda, Md., formerly worked for Fannie Mae and “frequently” used its name in his fraud pitch. His companies, Garfield Taylor Inc. and Gibraltar Asset Management Group LLC, were charged by the SEC, as were five alleged “collaborators”: Maurice G. Taylor of Bowie, Md., who is the brother of Garfield Taylor; Randolph M. Taylor of Washington, D.C., who is the nephew of Garfield Taylor; Benjamin C. Dalley of Washington, D.C., who is the childhood friend and business partner of Randolph Taylor; Jeffrey A. King of Upper Marlboro, Md., whose sister is married to Maurice Taylor; William B. Mitchell of Middle River, Md.

The scheme operated “at least” between 2005 and 2010, targeting “middle class” investors and charities.

The FDIC’s name was used to sanitize the scam.

Unregistered brokers were used to recruit investors.

The firms themselves were not registered.

Misleading PowerPoint presentations were used.

A Baptist church in Maryland, a children’s charity in Washington and an investment club in Philadelphia were shown the PowerPoint presentations.

Fancy language such as “proprietary strategy,” “covered call investment strategy” and “unparalleled downside protection” was used.

The Baptist church also was shown a “fake ‘letter of recommendation’ from Charles Schwab.”

“This letter was not prepared by anyone at Charles Schwab. Rather, it is a fabrication.”

A retiree from Lanham, Md., plowed more than $780,000 into the scam, an amount that represented “nearly his entire retirement savings.”

At least one investor in 2009 was worried about his/her nest egg in the post-Bernard Madoff environment, but Dalley reassured the investor that the opportunity had “taken the internal measures to strictly regulate our traders and accounting to ensure that our investor’s investments are safe.”

When Dalley provided the assurance, he already knew that the opportunity “had not followed a covered call trading strategy and had instead engaged in highly speculative naked options trading.”

Garfield Taylor actually was operating a “joint Ponzi scheme” through his companies.

Garfield Taylor “convinced at least three individuals to give him the username and password to their online brokerage accounts in order for Garfield Taylor to place trades in those accounts on a discretionary basis in exchange for a share of any profits generated.” A Maryland woman duped in this fashion lost “nearly her entire account” originally worth $450,000 “in a matter of two months.”

Garfield Taylor used investors’ money to send his children to private school at a cost of $73,000.

At one point, one of the Garfield Taylor firms had “less than” $1,000 in its account, but an investor “wired approximately $590,000.” Garfield Taylor used the incoming money to make Ponzi payments.

3.) Jamie Campany, 48, of Palm Beach County, Fla., sentenced to federal prison in $29.5 million fraud.

Key allegations:

More than 1,400 investors defrauded.

Multiple companies operating in South Florida and elsewhere involved, including Global Bullion Exchange LLC of Lake Worth. Scam also used name of “Barclay.”

Fraud fueled by telemarketing.

FBI, U.S. Postal Inspection Service and Florida Office of Financial Regulation handled probe.

John Mattera: Source: Mattera Foundation Nov. 2. 2011, news release

EDITOR’S NOTE: So, you recognize the power of the names of Groupon and Facebook and want to trade on their magnetism to drive traffic to your purported “opportunity” — and you want to further sanitize your scheme by describing yourself as a philanthropist and trading on the name of a charity such as the American Red Cross?

And you perhaps want to give money from your scheme to your wife and your mother, a senior citizen?

What follows is a story about the allegations against John Mattera and some of his activities in Florida . . .

John A. Mattera of Boca Raton, Fla., pleaded guilty in 2003 to seven counts of grand theft in three separate Florida criminal cases, according to court records. Among other things, “Mattera stole $34,000 from two Florida investors by promising to provide them with shares of stock that Mattera falsely represented he owned,” the SEC said of the 2003 cases.

In 2009, the SEC charged Mattera “with fraudulently attempting to avoid registration requirements by backdating promissory notes to obtain improperly unrestricted shares of a company,” according to the agency.

And now Mattera, 50, has been sued civilly by the SEC and charged criminally by federal prosecutors in New York in yet another alleged scheme — this one involving claims that Mattera traded on the names of Groupon, Facebook and others in a scam that netted between $11 million and $12.6 million.

The SEC said it is seeking an emergency court order to freeze the assets of Mattera; John R. Arnold, 61, of Florida; Joseph Almazon, 22, of Hicksville, N.Y.; David E. Howard II, 32, of New York City; Bradford Van Siclen, 43, of Montclair, N.J., and eight different business entities. (Ages in this paragraph approximate.)

Authorities said Mattera and “cohorts” duped investors into believing that they could convert shares in Mattera’s purported hedge fund — a company that happened to be pushed by “a web of registered and unregistered broker-dealers” — into shares of companies such as Groupon and Facebook in advance of the famous firms’ IPOs.

Both the SEC and federal prosecutors used descriptive verbs when describing what is alleged to be Mattera’s latest scam — a scam that allegedly involved a network of associates and a company with the high-sounding name of “The Praetorian Global Fund.”

(Emphasis added to SEC’s choice of verbs.)

“By conjuring up a seemingly prestigious hedge fund and touting the safety of an escrow agent, these men exploited investors’ desire to get an inside track on a wave of hyped future IPOs,” said George S. Canellos, director of the SEC’s New York Regional Office. “Even as investors believed their funds were sitting safely in escrow accounts, Mattera plundered those accounts to bankroll a lifestyle of private jets, luxury cars, and fine art.”

(Emphasis added to U.S. Attorney’s choice of verbs and other descriptors.)

“As alleged, John Mattera duped investors into believing they had bought rights to shares of coveted stock in Facebook and other highly visible and attractive companies which had not yet gone public,” said U.S. Attorney Preet Bharara of the the Southern District of New York. “As the complaint describes, Mattera told elaborate lies about stock he did not own and about how he would keep investors’ money safe in escrow accounts. Instead, Mattera took the investors’ money to fund his own extravagant lifestyle. With today’s charges, his charade is exposed and he will be held to account for his alleged crimes.”

Named relief defendants in the SEC case are Ann Mattera, Mattera’s 71-year-old mother, and Lan T. Phan, Mattera’s wife. Phan, 43, is a physician and yoga practitioner. Authorities say the women, who are not charged with an offense, were beneficiaries of the scheme. (Ages in this paragraph approximate.)

The publicity surrounding John Mattera’s alleged business misdeeds has caused embarrassment for a local chapter of the American Red Cross in South Florida. John Mattera, who is linked on the web to numerous companies or philanthropic organizations even in the wake of previous lawsuits and criminal charges against him, was on the Red Cross board in Broward County until last month, according to the Sun-Sentinel.

On Nov. 2, just days before the SEC and the Feds came knocking, John Mattera was quoted in this news release about an entity known as the Mattera Foundation, which purported to look “to support those in need” by making it easier for them to find grant funding.

“John Mattera hopes that organizations across South Florida will use the new grant application tool to contact The Mattera Foundation and secure funding for their causes,” the news release read in part.

On March 24, 2011, meanwhile, John Mattera was quoted in this news release about a Red Cross golf tournament sponsored by the Mattera Foundation.

From March 2011 news release by the Mattera Foundation.

“Investor and American Red Cross board member John Mattera announced today that his eponymous The Mattera Foundation will sponsor the upcoming American Red Cross Golf Tournament,” the release read in part. “The tournament will be held at the Inverrary Country Club on April 1, and all proceeds will benefit the American Red Cross, South Florida Region.”

It was not immediately clear if Mattera plowed investors’ money into charities. What is clear, according to federal prosecutors, is that he had high appetites and caused investors to believe their money was going into escrow accounts.

“Based on the misrepresentations of Mattera and others, investors sent more than $11 million into escrow accounts maintained at a Florida bank,” prosecutors charged. “Mattera reassured investors that their money would be held in the escrow accounts until either the offering was completed or another triggering event took place, at which time the investors would receive their ownership interest in the particular special purpose entity. However, instead of maintaining the investor money in the escrow accounts as he promised, Mattera caused the vast majority of it to be transferred to other entities with which he was associated. Ultimately, Mattera misappropriated more than $11 million of investor money and spent nearly $4 million on personal items for his family and himself, such as expensive jewelry, interior decorating and luxury cars.”

A veteran IRS agent also used strong language when describing Mattera’s latest alleged fraud scheme. (Emphasis added.)

“The allegations against Mr. Mattera show that the appearance of success can be a tangled web of financial lies,” said Victor W. Lessoff, special agent-in-charge of the Newark (N.J.) Field Office of the IRS Criminal Investigation Unit (IRS-CI).

Such descriptions also surfaced in the epic Scott Rothstein Ponzi caper, which also operated in South Florida.